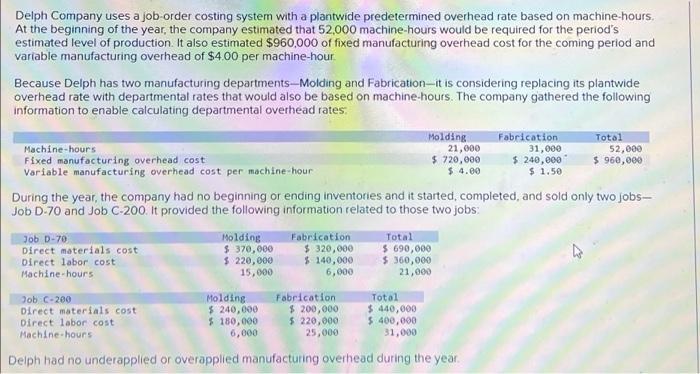

Delph company uses a job-order costing system – In the realm of accounting, Delph Company stands out as a prime example of the successful implementation of a job-order costing system. This system empowers Delph Company to meticulously track and allocate costs, ensuring accurate job costing and informed decision-making.

Job-order costing, a specialized costing method, plays a pivotal role in industries where production involves distinct and identifiable jobs or batches. Delph Company, operating in such an industry, has harnessed the capabilities of job-order costing to gain a competitive edge.

Overview of Job-Order Costing System

Job-order costing is a costing method used by companies that produce unique or customized products or services for each customer. It tracks costs associated with each individual job, providing insights into the profitability and efficiency of specific projects.

Key Elements and Processes

- Job Cost Sheet:A document that tracks the costs incurred for each job.

- Direct Costs:Costs that can be directly traced to a specific job, such as materials and labor.

- Indirect Costs:Costs that cannot be directly traced to a specific job, such as factory overhead.

- Cost Accumulation:The process of gathering and assigning costs to each job.

- Cost Assignment:The process of allocating indirect costs to specific jobs based on a predetermined method.

Industries Using Job-Order Costing

- Construction

- Manufacturing

- Engineering

- Custom furniture making

Delph Company’s Implementation of Job-Order Costing

Delph Company has implemented a comprehensive job-order costing system to track the costs associated with its custom furniture projects. The system involves the following procedures:

- Job Cost Sheet Creation:A job cost sheet is created for each new project, including details such as customer name, project description, and estimated completion date.

- Cost Collection:Direct costs, such as materials and labor, are recorded on the job cost sheet as they are incurred.

- Indirect Cost Allocation:Indirect costs, such as factory overhead, are allocated to each job based on a predetermined overhead rate.

- Cost Reconciliation:At the completion of a job, the actual costs incurred are compared to the estimated costs, and any variances are analyzed.

Unique Aspects

- Delph Company uses a cloud-based job costing software that allows for real-time cost tracking and reporting.

- The company has implemented a system of job costing codes that facilitate the accurate allocation of costs to specific projects.

Advantages and Disadvantages of Job-Order Costing: Delph Company Uses A Job-order Costing System

Advantages

- Improved Cost Control:Provides detailed information on the costs associated with each job, enabling managers to identify areas for cost reduction.

- Accurate Product Costing:Helps companies determine the actual cost of producing each product or service, ensuring accurate pricing and profitability analysis.

- Enhanced Decision-Making:Provides insights into the profitability of specific projects, aiding in decision-making regarding resource allocation and project selection.

Disadvantages, Delph company uses a job-order costing system

- Increased Complexity:Job-order costing can be complex to implement and maintain, especially for companies with a large number of unique projects.

- Potential for Errors:The manual nature of job-order costing can lead to errors in cost accumulation and assignment.

- High Cost:Implementing and maintaining a job-order costing system can be expensive, particularly for small businesses.

Cost Accumulation and Assignment

In a job-order costing system, costs are accumulated and assigned to specific jobs as they are incurred. Direct costs, such as materials and labor, are easily traceable to specific jobs and are directly charged to the job cost sheet.

Indirect Cost Allocation

Indirect costs, such as factory overhead, cannot be directly traced to a specific job. Therefore, they are allocated to jobs based on a predetermined method. Common allocation methods include:

- Direct Labor Hours

- Machine Hours

- Units Produced

Delph Company’s Cost Assignment

Delph Company uses a combination of direct labor hours and machine hours to allocate indirect costs to jobs. This method ensures that the indirect costs are fairly distributed based on the resources consumed by each job.

Job Cost Sheets and Work-in-Process Inventory

Job Cost Sheet

A job cost sheet is a document that tracks the costs associated with a specific job. It includes the following information:

- Job number

- Customer name

- Project description

- Direct costs

- Indirect costs

- Total cost

Work-in-Process Inventory

Work-in-process inventory (WIP) refers to the costs of jobs that are still in progress. In a job-order costing system, WIP is recorded at the end of each accounting period to reflect the costs incurred on incomplete jobs.

Cost Reconciliation and Variance Analysis

Cost Reconciliation

Cost reconciliation is the process of comparing the actual costs incurred on a job to the estimated costs. This helps to identify any variances between the two and determine the reasons for the variances.

Variance Analysis

Variance analysis involves investigating the causes of the variances identified during cost reconciliation. Common types of variances include:

- Material Price Variance:Difference between the actual and standard price of materials.

- Material Quantity Variance:Difference between the actual and standard quantity of materials used.

- Labor Rate Variance:Difference between the actual and standard labor rate.

- Labor Efficiency Variance:Difference between the actual and standard labor hours required to complete a job.

Delph Company’s Variance Analysis

Delph Company regularly conducts variance analysis to identify areas for cost improvement. The company uses the results of the variance analysis to make informed decisions regarding production processes, resource allocation, and pricing strategies.

FAQ Guide

What is the primary purpose of a job-order costing system?

A job-order costing system primarily aims to accumulate and assign costs to specific jobs or batches, providing detailed information about the costs incurred in each production order.

How does Delph Company utilize job-order costing?

Delph Company employs job-order costing to track costs associated with each unique production job. This enables the company to determine the profitability of individual jobs and make informed decisions regarding pricing and resource allocation.

What are the key advantages of job-order costing for Delph Company?

Delph Company benefits from improved cost control, accurate job costing, and enhanced visibility into production costs through the implementation of a job-order costing system.